Fish, Bananas, & Comparative Advantage, Apropos of Nothing

A post definitely not about current events.

When I was an undergraduate, I volunteered to be a subject in a behavioral economics experiment. I never found out which faculty member was doing the research, but my guess is that it was Robert Frank, who would later pen excellent books such as Passions Within Reason and The Darwin Economy.

I came into the lab and was provided with a set of simple instructions. I was provisionally allocated $10, and I had to divide it with a person in a different room. My role in the game was to be “the proposer.” I had to write a number between $0 and $10 on a piece of paper. This was the amount of money I would be “proposing” to give to the other person, called the “Responder.” If the Responder accepted my proposal, then we would walk out with the cash as specified in my proposal. But if the Responder rejected it, we would both get nothing. You will likely not be surprised to learn that this is referred to as “the ultimatum game.”

I was, to be sure, a bit behind the curve in terms of my overall social intelligence and, worse, was already trained to think like an economist. So, I reasoned that from the Responder’s perspective, her choice would be between $0 and whatever I offered her. So if I proposed a $9/$1 split, she would take it because rejecting it would be irrational. Irrational! The option of $0 is “strictly dominated,” in the language of economics, which in this case just means $1 is better than $0.

So I made my proposal and exactly what you think happened, happened.

I recently argued that humans—holding me aside—have pretty good intuitions about the social world. We are, after all, a very social species, descended from those humans who deftly navigated the complexities of the toughest part of the ancestral environment: other humans.

Having said that, our minds are not designed to deal with very recent aspects of the world, especially those created by new technologies. So we can digest the import of the subtlest changes in facial expressions, but fail to adequately process the mortality risks of texting while driving. (See the post by Josh on, well, all his posts for more on the topic of mismatch.)

Now, humans are pretty good at dealing with trade and exchange. John Tooby and Leda Cosmides’ work on cheater detection and social exchange makes that point.

A problem, however, is that in some sense, our nose for cheaters is too sensitive. We are very quick to see situations as competitive—with winners and losers—even when they are not. This perception is because fitness is zero-sum—if one person gains then someone else necessarily loses—so many of our economic intuitions reflect the operation of this lens. Once we see an interaction through these competitive lenses, we see others’ gains as our loss. This makes sense in a world in which one is competing with, well, pretty much everyone.

These intuitions don’t serve us as well in a world with trillions of dollars of international trade. I like the way that Pascal Boyer and Michael Bang Petersen put it, that people’s intuitions about economics “often conflict with elementary principles of economic theory.”

That’s a polite way of saying that people really suck at basic economics.

In particular, they argue that when it comes to international trade, lay people believe that “a nation should always try to export more goods than it imports” and that people generally assume, working in the title of Adam Smith’s famous work, that “the wealth of nations is the outcome of a zero-sum game. As a consequence, the fact that foreigners profit from trade entails that ‘we’ are losing out.” Indeed, research has shown that many people think that if a country imports goods that it could, in principle, manufacture, then trade is a cost not a benefit. As I try to illustrate with fishes and bananas below, it is not.1

This idea takes us back to the opening vignette. Here is how my former mentor John Tooby and collaborators put it. (Translation from academese follows the quote.)

The evolved aversiveness of low payoffs in interactions should be a function of comparative payoff, not just absolute payoff. In rational choice theory, any payoff is better than no payoff, but in the evolutionary competition of alternative designs, a positive absolute payoff that is a low relative payoff should (under many conditions) be selected to be perceived as worse than a zero absolute payoff that is equally bad for both participants.

That is, we naturally see someone else getting a better outcome than us as bad, even if the alternative is that we get nothing at all. In the context of international trade, Boyer and Petersen argue that people (without economic training) see exchange as competitive rather than cooperative, and they apply this not only to individuals, as in the ultimatum game, but to groups. Again, as they put it, when it comes to trade, “there is a strong prior belief that any advantage to another group is detrimental to one’s own.”

Look, it took brilliant people such as Adam Smith and, the subject of the balance of this post, David Ricardo, to think through international trade carefully. It is a bit counterintuitive.

At the start of the 19th century, the industrial revolution was blooming and international trade was expanding. Rulers were tempted to erect trade barriers—tariffs, duties, quotas, etc.—to increase the price of foreign goods, making domestic goods more competitive. So if corn was being imported into England from Poland, tariffs could increase the price of Polish corn, making English corn more competitive. At the time, it wasn’t well understood what the consequences of such policies would be.

In his book On the Principles of Political Economy and Taxation published in 1817, David Ricardo made the (counterintuitive) claim that countries were better off specializing in producing goods in which they had a comparative advantage—see below—even if the country was less efficient at producing that good than its trading partners. Paul Krugman referred to this notion as “Ricardo’s difficult idea.” Krugman writes, “The idea of comparative advantage -- with its implication that trade between two nations normally raises the real incomes of both -- is, like evolution via natural selection, a concept that seems simple and compelling to those who understand it. Yet anyone who becomes involved in discussions of international trade beyond the narrow circle of academic economists quickly realizes that it must be, in some sense, a very difficult concept indeed.”

So, apropos of absolutely nothing in particular that has been happening in the world, I’d like to try to explain Ricardo’s insights into international trade in a way that I hope makes it easier to see what he was arguing.

To get at the complexities, I’m going to simplify wildly, as economists tend to do, to try to get to the core idea. So here’s the story.

Once upon a time, Amanda and Bill were on a delightful cruise when the god Poseidon visited a tremendous storm upon their ship. Breathless, they washed ashore on an uninhabited island which, fortunately, had abundant bananas and plentiful nearby shoals where the fishing was good.

Amanda, a CrossFit athlete, is a machine: she can catch 3 fish per hour or pick 6 bananas per hour. Bill, who only does Pilates, is slower at both. He catches just 1 fish per hour or picks 4 bananas per hour.

You might think that Amanda should just fish and harvest for herself. After all, Amanda is three times the angler than Bill is and also 50% faster at harvesting bananas. That’s where Ricardo comes in.

We’re going to look at the economic output of Amanda and Bill in this simple fish/banana economy. (I prefer this to guns and butter. Less violent and more plausible for the desert island context.)

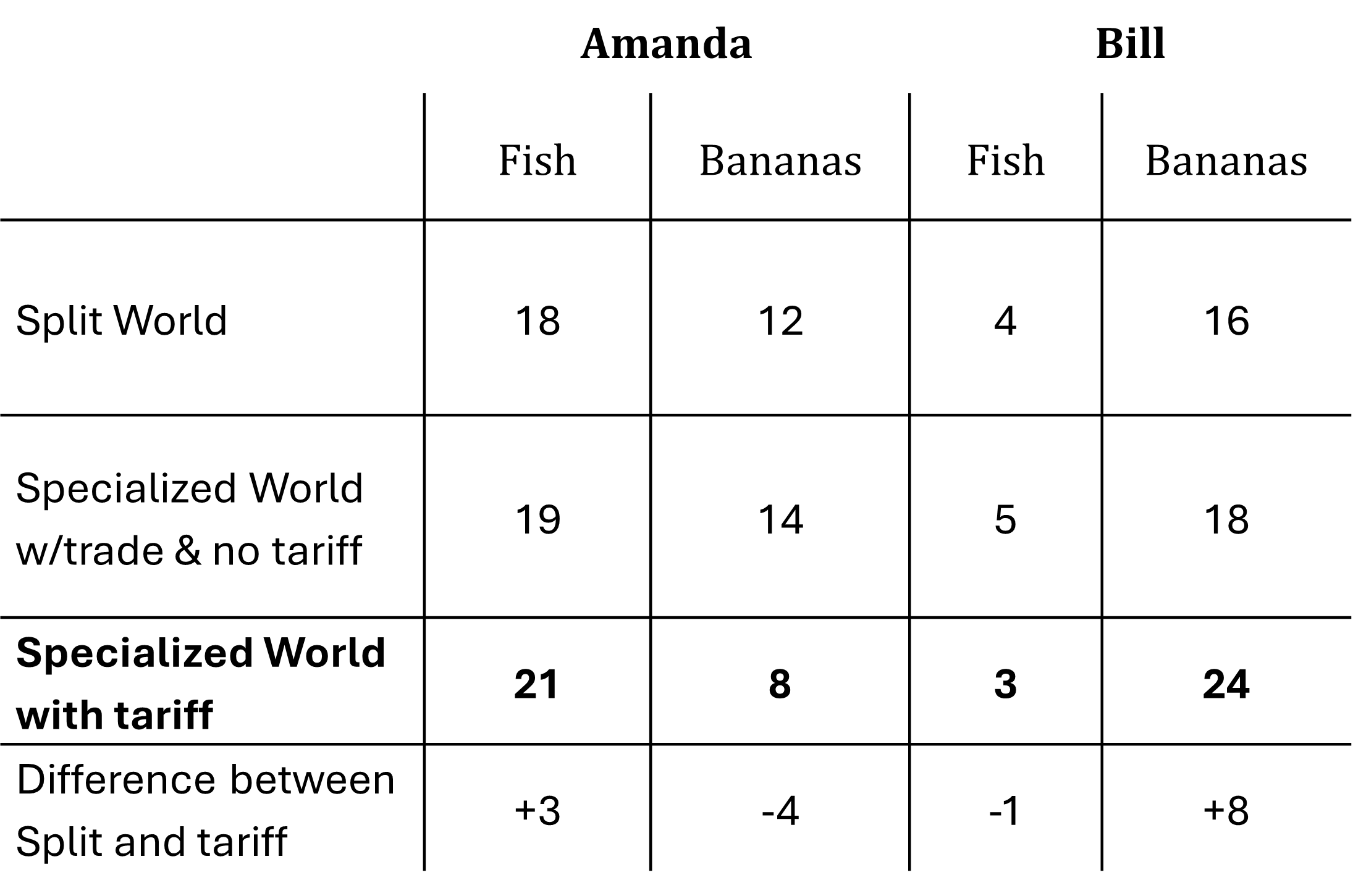

Ok, we assume that each person works 8 hours per day. Let’s compare two approaches. In the first one, both mix their daily activities. Amanda mostly fishes—she likes fish—and spends some time, just a couple hours, harvesting bananas. Bill splits his time evenly between fishing and picking. (The argument works if Amanda splits her time evenly. I picked numbers to make parts of the math come out nice.)

Here is the production of this economy, which I’ll call the Split Economy.

Amanda:

6 hours fishing → 18 fish

2 hours gathering → 12 bananas

Bill:

4 hours fishing → 4 fish

4 hours gathering → 16 bananas

Combining their output gives us the Gross Island Product (GIP). In this Split economy, the GIP is 22 fish, 18 from Amanda and 4 from Bill, and 28 bananas, 12 from Amanda and 16 from Bill.

Now we suppose that Amanda only fishes and Bill only gathers bananas. In this economy, the Specialized Economy, we get:

Amanda fishes: 8 × 3 = 24 fish

Bill gathers: 8 × 4 = 32 bananas

Combining their output gives us the island’s Gross Island Product with specialization. In this Specialized economy, the total is 24 fish and 32 bananas. Notice that specialization creates a surplus of 2 extra fish and 4 extra bananas.

But wait, there’s more.

Let’s add trade. Suppose Amanda gives Bill 5 fish in exchange for 14 bananas. These numbers seem a bit odd, but remember that both people get bananas about three times as fast as fish, so it’s pretty close to that. And these values divide the gains from trade equally.

Here’s how they end up:

Amanda:

24 − 5 fish = 19 fish

Gains 14 bananas = 14 bananas

Bill:

Gains 5 fish

32 − 14 bananas = 18 bananas

Let’s compare the specialized world with trade to the split world.

Specialization and trade isn’t a win-lose, as our intuitions sometimes tell us. It’s a win-win, made possible by doing what each person is comparatively better at, then trading. In this example each person is strictly better off, meaning that for both commodities, they have more than they did under the other condition. When everyone is strictly better off, that’s a big deal, economically. Nobody has less of anything that they value than they otherwise would.2

Crucially, this is true as much for Amanda as for Bill. Yes, Amanda is better than Bill at everything, but she’s more better, if you will, at fishing. One way to think about it is my favorite notion of opportunity cost. Amanda gives up only 2 bananas per fish (6 bananas ÷ 3 fish) while Bill gives up 4 bananas per fish (4 ÷ 1). So Amanda has a comparative advantage in fish, and Bill in bananas. By each focusing on what they give up least, they expand the total fish/banana pie.3

Ok, now let’s talk just a tiny bit about, again for absolutely no particular reason, tariffs.

The island, as it turns out, is governed by monkeys. They are large and, in both Amanda’s and Bill’s neighborhood, have the monopoly on the use of force, so they can dictate terms. They dictate, in fact, a 40% tariff (or duty) on trade.4 Specifically, the Amanda monkey administration declares that whoever sells bananas to their side of the island must pay a banana duty.

Amanda and Bill initially contracted 5 fish for 14 bananas. Bill prepares his 14 bananas to take to Amanda’s camp. The monkeys announce their tariff of 40%, rounding up to 6 bananas. So now Bill will have 8 bananas to trade. Amanda, now getting just 8 bananas, is unwilling to part with more than 3 fish. In Tariff World, if the trade goes through, the outcomes (in the bold row) are as follows:

This trade no longer makes the parties strictly better off. Depending on their preferences, they still might do it, but it’s less likely. The tariff doesn’t just reduce the total number of bananas or fish that the two people have—it prevents the trade from happening. (Of course, the monkeys get six free bananas if the trade does go through. So that’s nice for them. It turns out that monkeys squander free bananas when they get them, so we should be careful how we account for this monkey windfall.)

The lessons are as follows.

· Specialization and trade can make parties better off, even if one party is better (more efficient) at producing something it’s now trading for.

· Tariffs reduce the possible gains from trade.

· When trade is taxed—whether by banana duty, fish fee, or any other mechanism—a win-win can turn into a lose-lose. The incentive to specialize erodes. The gains from trade shrink. .

One last thing.

Charlie comes along and says, well, there’s something you have omitted. In your hypothetical, you yourself said the monkeys have a monopoly on the use of force. This analysis ignores other issues, including the potentially very important one of national defense. Sure, Amanda might fish all the time, but suppose the day comes when the Great Banana Battle dawns and Amanda has only a limp fish in her hand? The domestic banana industry must be protected, scream the monkeys.

Well, that might be true. But it’s worth making a few points.

The main one is that this is an economic analysis. Yes, it ignores that issue. So that’s fair.

Next, this concern makes sense to the extent that the industry is related to defense or some other strategic goal. If reduced banana capacity is a strategic liability, then, yes, it might make sense to take steps to reduce that threat. So one might say that if your power to levy duties is based on a defense justification, then the products you assess better have something to do with national defense.

The next question is whether tariffs are the right way to protect banana production. They might be. There might be better ways.

For instance, instead of a tariff, the monkeys on Amanda’s side of the island might subsidize banana production. With the right subsidies, Amanda might maximize her outcomes by mixing her production of the two commodities. Along similar lines, if bananas are a strategic defense resource, Amanda’s monkey government could contract to buy them from her, perhaps paying a higher-than-market price, maybe one fish for only two bananas. This could distort the banana market, but maybe not by much; after all, if the monkeys have a genuine demand for bananas, that should be reflected in the price. Related, the monkeys could incentivize researching banana productivity technology. Perhaps with better technology, Amanda could harvest more rapidly, making it economically viable.5

In terms of budgeting, if the monkeys do implement these sorts of programs, one might think of these programs as national defense budget costs. It’s not irrational for the monkeys to get together and spend money for defense. The world is a dangerous place.

Another route is to work hard to cultivate alliances with other banana producers. Instead of alienating allies, one might work with them, developing contingency plans, perhaps with banana futures contracts. The more nations island economies there are, the easier it is to solve this problem with trade with allies. This assumes that one doesn’t scuttle one’s alliances.

With, say, aggressive tariffs.

Now, none of this has anything to do with current events.

I’m just saying, humans have bad evolved intuitions about economics, seeing competition and zero-sum interactions everywhere—some seeing them more than others, no doubt—and can, therefore, make mistakes.

While many human intuitions are good, we need good (time-tested) theories to fill in the gaps where they are not.6

Optional CODA

An exercise for the reader. This post is already longer than our usual and you won’t miss anything if you skip this little postscript. But read on if you were wondering how current account deficits apply to these economies.

Suppose the monkeys on Amanda and Bill’s island start using rare shells as a medium of exchange.7 They will give you, say, one such shell for a banana and three such shells for a fish. They might also give you bananas and fish in exchange for shells at these rates.

Imagine another island, where they hunt for lobsters and harvest coconuts. It turns out that Amanda and Bill really like these goods. The people on the other island accept Bill and Amanda’s fancy shells, earned in the local economy, in exchange for the other island’s goods.

Every year Amanda and Bill trade with the other island and wind up buying a bit more from the other island than they sell. The shell system is used by, in fact, many islands. So every year, there are 10 fewer shells on their island. Thankfully, the monkeys find a lot of shells every year. Actually, they can turn regular shells into fancy shells with only a little time and trouble.8

From Amanda and Bill’s perspective, they get all the coconuts and lobsters they can afford by trading their shells. From the perspective of the island, as a whole, it is down, net, some shells every year but enjoys coconuts and lobsters. Other islands might be accumulating shells over time.9

How worried should Amanda, Bill, and the governing monkeys be about the shell deficit? Why?

I make the usual assumptions that economists make in all of this. I omit transaction costs, the costs of switching from producing one good to producing another, changing preferences, and so on.

For the technically inclined, this is a Pareto improvement.

Mmmm…. fish banana pie…

This number was of the moment when this was drafted, but has been overtaken by events.

Yes, direct subsidies, government purchases, and research subsidies might annoy trading partners. No one said that all of this was easy.

And a store of value and a unit of account. #IYKYK

The process involves a plant called a “mint.”

Note that it’s true that you can think of those shells as claims on goods and services, so, yes, it’s fair to say that these are not just shells.

thanks, save me writing (badly) a version of this...

Thanks for the education, Rob! I understood this in principle, but never bothered with the math!